This article is about the United Kingdom coffee culture: From Tea To Speciality Coffeer: From Tea To Speciality Coffee. The second wave’s success was much more pronounced in markets where coffee was not the most popular beverage. Even among them, though, historical meanings have been harnessed to aid in the structuring of modern consumption. Although the originator of the early European coffee shop, the United Kingdom has long been a tea-drinking society.

The industrial revolution established inexpensive tea as the workers’ preferred beverage, supplied by plantations across the Empire, notably those in Ceylon was switched from coffee-growing after being ravaged by coffee rust in the second part of the nineteenth century.

Domestic coffee consumption only truly took off in the 1950s, thanks to the development of “instant,” or soluble, coffee products. Their early success was due in large part to the introduction of commercial television, since, unlike a pot of tea, they could be brewed in the time allotted for an advertisement break. Tea manufacturers retaliated by inventing the teabag (Bramah, 1972).

After the first Gaggia machine was placed in a coffee bar in London’s Soho entertainment district in 1952, the 1950s witnessed a brief resurgence of out-of-home coffee shops. By 1960, it was estimated that there were 500 in London and 2000 throughout the country. Their success was due to the fact that they became places for teens to mingle and, in particular, listen to and dance to music, whether live or from a jukebox, without having to meet their parents at the bar (Clayton, 2003).

Despite the lack of emphasis on coffee quality, this built a strong link between coffee and Italy in the British mind, which was bolstered by the high number of Anglo-Italian employed in the catering industry. Many restaurants just provided “frothy coffee,” which was essentially any type of coffee base (even soluble) topped with frothy milk, which could be presented as a “cappuccino” after chocolate sprinkles were added (Morris, 2005). However, by the mid-1960s, coffee shops were dwindling as pubs began to attract younger patrons.

When local businesses began to adopt the coffee shop concept that had grown in the United States for the United Kingdom in the 1990s, the significance of this became obvious. They considered branding as a vital component of this since it would help them stand out from the existing sandwich shops and cafes, allowing them to charge the all-important premium for the coffee beverage that backed the business model.

Several, such as the Seattle Coffee Company, which launched what is widely considered as the first London coffee shop in 1995 and sold its 65-store network to Starbucks in 1998, elected to portray themselves as American. Similarly, the Coffee Republic, which opened in the same year, intended to hire baristas among American students studying abroad (Morris, 2013c).

Branding of three major United Kingdom coffee shops

Instead of positioning themselves as Italian in their proposal, the two most enduringly successful local chains, Costa and Cafe’ Nero, structured their appeal to British understandings of coffee and the goal for a “continental cafe’ culture.” Costa, for an instance, could draw on its history as a company founded by two members of the Anglo-Italian community in the 1970s and used this to explain slogans like “Italian about Coffee,” rather than the reality that it was now controlled by the Whitbread leisure conglomerate.

Cafe’ Nero had no such history to draw on, but it didn’t hesitate to call itself “the Italian coffee company,” aiming to convey this in part through the more edgy, dark wood interiors of its establishments, and, most famously, by permitting smoking until the law was changed in 2007. However, rather than the upright sip-and-go model of the Italian espresso bar, both Nero and Costa use the coffee shop format of “dwell friendly shops.”

Instead, they provided a totally Italian coffee experience, with any client demands for “regular coffee” being handled by pouring Americanos. Both utilized espresso blends with a percentage of Robusta that were produced on “classic” Italian-made equipment. People understood that if they came to Nero, everything would revolve around espresso, as Paul Ettinger, the first Food and Beverage Director, said.

People knew if they came to Nero, it was all going to be around espresso. We never did any drip coffee. never tried to be smart, we didn’t do the big American jugs, we didn’t do the gimmicks, the syrups, so we were early on very pure. an Italian coffee bar.– Interview cited in Morris (2013c, p. 890)

Customers appear to have responded well to these branding initiatives. Costa, Starbucks, and Cafe’ Nero were the three largest coffee shop chains in the United Kingdom as of December 2015. Costa had 1922 locations, Starbucks had 849, and Cafe’ Nero had 620. This represents 53% of the branded coffee shop market, but only 17% of the total number of specialty coffee outlets in the United Kingdom, which totals 20,728.

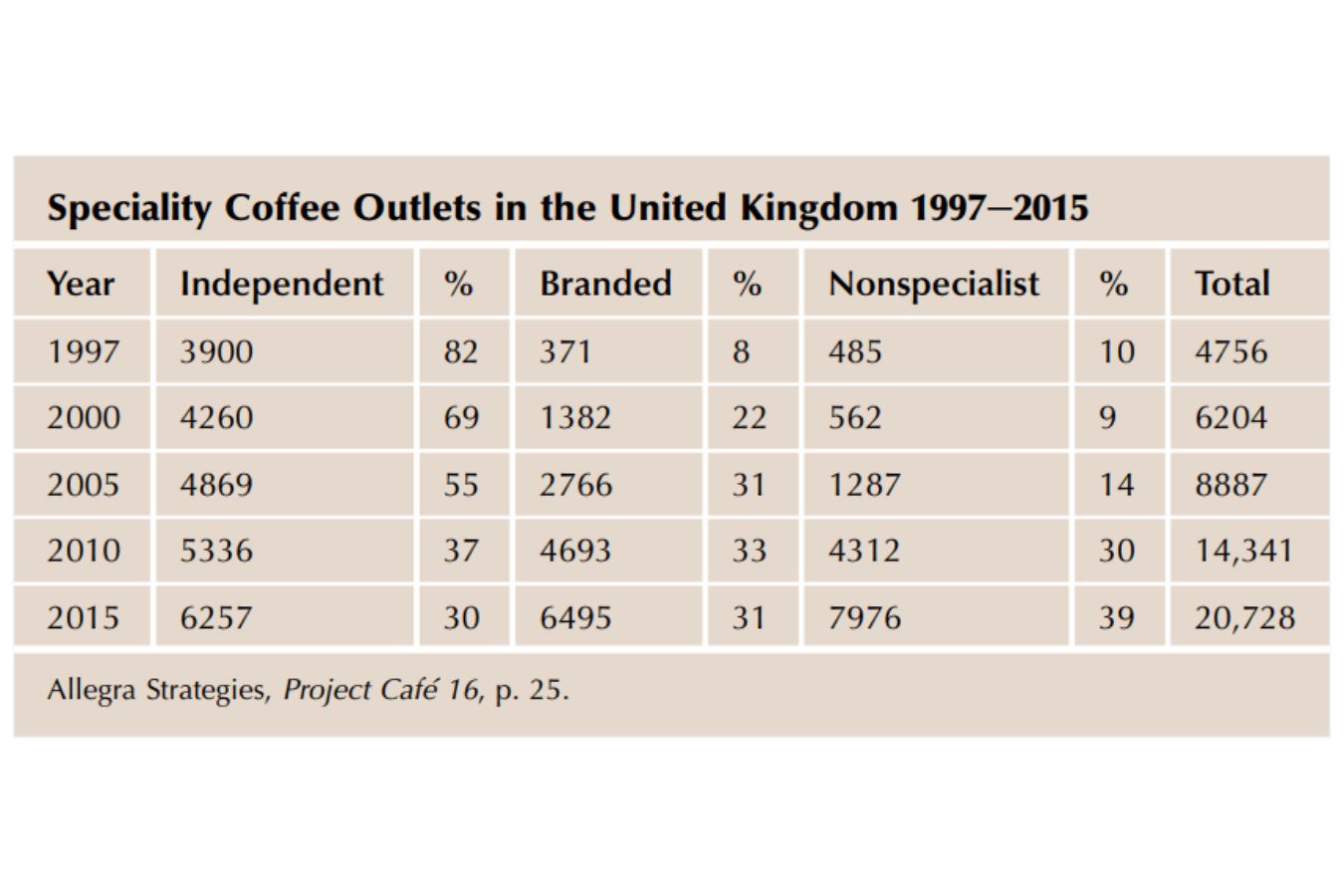

Allegra Strategies, the most carefully followed market research firm in the coffee business, has been following the growth of the United Kingdom Coffee market since 1997 and has graciously provided the data on which the following study of United Kingdom consumer habits is based (Allegra, 2016). Since Allegra began tracking the industry, the number of establishments offering specialty coffee, defined as handcrafted espresso-based drinks, has more than tripled.

Building specialty coffee

Within this general boom of coffee culture, many stages of growth may be differentiated. Although independent operators dominated the little offering available in 1997, branded chain operators were the driving force for expansion, increasing their outlet share from 8% to 31% by 2005.

Nonspecialist operators, such as department store cafes, supermarket cafes, pubs, motorway, and forecourt coffee shops, and quick-service restaurants, have subsequently moved to include specialty coffee on their menus, increasing their proportion of outlets from 14 percent in 2005 to 39 percent in 2015. Their domination in the market reflects a larger trend in the United Kingdom: specialty coffee has gone mainstream.

Espresso-based drinks have become the go-to coffee choice outside the house for the British consumer. Customers choose latte, cappuccino, and americano at coffee shops, with latte being three times more popular than tea. The fact that “functional” reasons such as “need to have a coffee” dominate consumer motives for visiting a coffee shop, and convenience is still regarded as the key selection factor, may explain why coffee consumption and coffee shops have become mundane elements of United Kingdom coffee culture.

The most frequently mentioned handy location, however, is one near shopping centers, indicating how coffee has been ingrained as a home habit.

There are some fascinating gender and age disparities to be found. Women are significantly more likely than males to utilize a coffee shop visit to socialize (29 percent vs. 17 percent), and as a result, they are more likely to visit in the afternoons, on weekdays later in the week, and to stay longer. Men are more likely to attend on a daily basis and in the early morning, implying that coffee is a part of their daily routine.

Similarly, while customers aged 25 to 44 are most likely to visit early in the mornings and are the most frequent takeaway customers, those aged under 24 are most likely to visit in the afternoons and have the highest propensity for socializing, studying, and using Wi-Fi, while those aged 65 and up visit in the mid-mornings have the longest dwell times of all.

These disparities show that different consumer groups have different habits that enable them to incorporate coffee shop use into their daily routines.

Nonetheless, there have been some noticeable shifts in consumer incentives and behaviors since the mid-2000s financial crises. The importance of convenience as a motivator of coffee shop choice has significantly decreased, but the importance of coffee quality has grown, as has loyalty to both operator and coffee supplier brands, as well as the patronage of a single favorite coffee shop.

This is especially true among frequent specialty coffee drinkers. There are strong indications that this is due to a growing interest in so-called third-wave coffee, as evidenced by much higher consumer “promoter” scores for independent operations and consumer households with 33 percent owning pod machines and 7% owning artisan brewing equipment like an Aeropress or V60.