Coffee Derivatives Market: In the formation, existence, and development process, the world economy has undergone inevitable stages of evolution from self-sufficiency to simple commodity production, in which commodity exchange has changed from exchanging goods into cash transactions. Each inventive step is a significant turning point in the economy, marking a step-by-step change and perfection in human behavior and perception. Today, when science and technology have developed rapidly, the exchange of goods is no longer paid in cash but also in contractual agreements, whereby the time and place are determined—determined in the future.

Today, commodity trading tends to be carried out on the commodity derivatives market, with specific financial instruments such as coffee, rubber, cocoa, pepper, etc. Although this market was established not long ago and needed to become more popular than traditional cash transactions, this is considered a new direction for domestic and international businesses.

The form of trading by derivatives creates a hedge to limit business price risks and reduce the time and cost of searching the market. To gain more profit or to avoid contractual obligations when not wanting to own the agreed goods, contracts can be passed many times before the contract expiration date.

2005 – 2006 is considered the first period to apply the derivatives market to Vietnam through futures contracts, and one of the commodities traded on the market is coffee.

Vietnam is the world’s second-largest coffee exporter, with quality tested according to international standards, but the country’s export coffee price is only 65-85% of the coffee export price of other countries; Because domestic coffee businesses have not determined long-term business plans, coffee is mainly sold in bulk at the beginning of the season, creating opportunities for buyers to pressure prices.

Therefore, the coffee derivatives market is expected to be a new direction in solving output for the coffee industry, stabilizing selling prices and minimizing risks of the trade, creating a relatively stable business environment in terms of prices., encouraging Vietnamese businesses and farmers to focus on production and effectively exploit the benefits that coffee brings.

Today, Helena Coffee Vietnam with Mr. Edison Nguyen (Vice Director of Helena., JSC) will provide an overview of the development process of the derivative coffee market in the world and Vietnam and the orientation to develop the Vietnamese coffee derivatives market in the coming time.

Overview Of The Coffee Derivatives Market

The derivatives market is where the signing and trading of derivative products occur. A derivative product is a financial product whose result is created from developing another product, also known as the underlying asset (the underlying asset can be a bond, stock, currency, or goods). The value of the derivative is determined based on the volatility of the underlying asset’s value. Derivatives transfer undesired risk to counterparties who either have the risk offset or wish to assume that risk.

What Is the Coffee Derivatives Market?

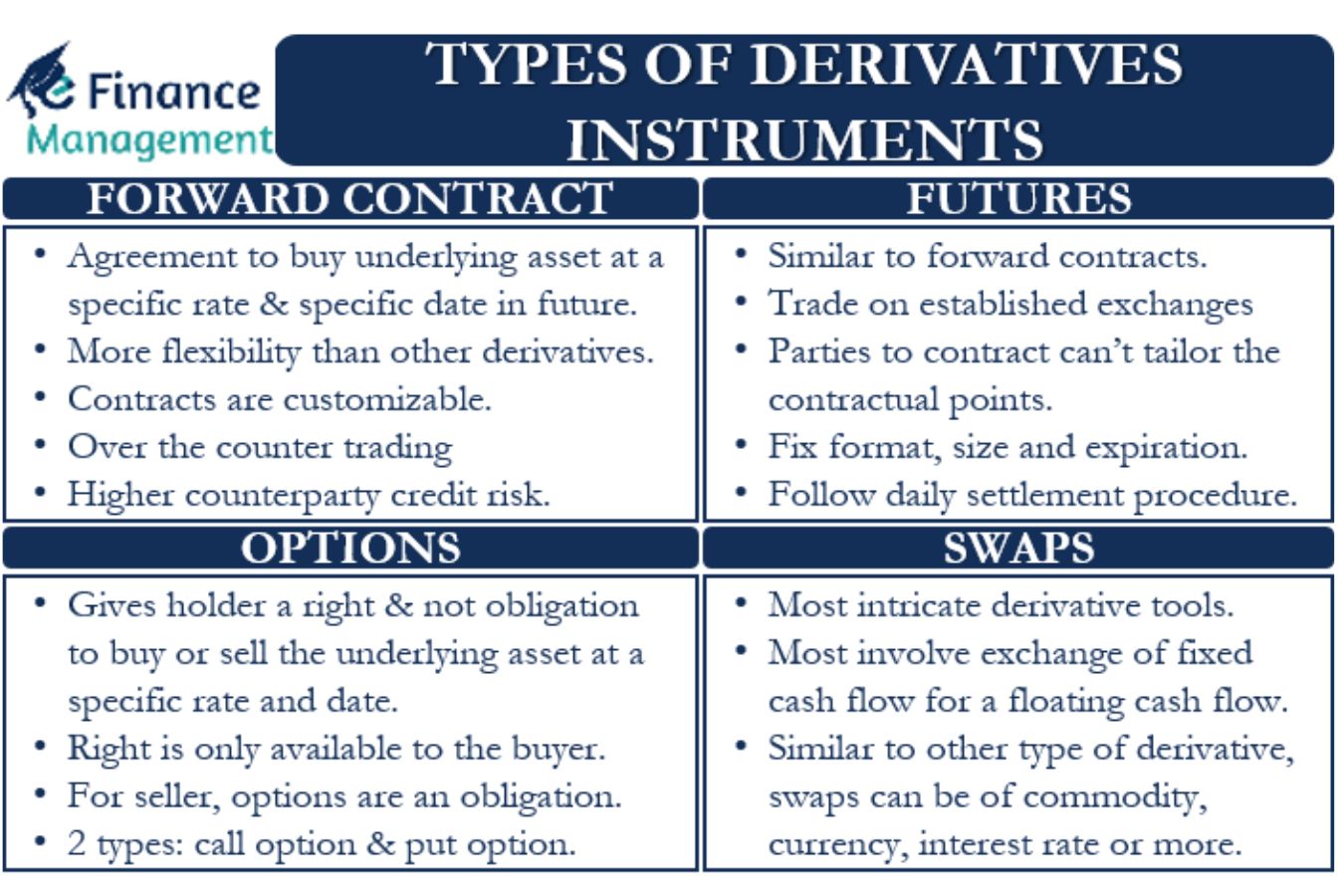

Basic types of coffee derivatives: The coffee derivatives market includes contracts such as forwards, futures, options, and swaps.

Forward contract

* Definition: A forward contract is a contract signed between a buyer and a seller at present, but the performance of the contract will take place at a future time. The value of the forward contract is delivered only on the contract maturity date; no payments are made on the date of signing or during the contract term.

* Features:

- Conducted through the informal market (OTC).

- Not according to the standards of the market; flexible agreement terms.

- High liquidity risk because it is difficult for the parties to sell the contract.

- High risk of settlement because at maturity, both parties will transact at a predetermined price, whether the market price is higher or lower than the price specified in the contract.

Forward contracts are usually based on a trusting relationship between the parties.

Future contract

* Definition: A futures contract is a standardized forward contract traded on an exchange. The contract value is market-adjusted daily, in which one party’s losses are paid out to the other.

* Features:

- Contracts are traded at the exchange through intermediaries who are brokers.

- Standardized futures contract terms.

- Futures contracts must have the same margin for both the seller and the buyer.

Most futures contracts are liquidated ahead of time.

Option contract

Definition: An option is a contract between a buyer and a seller in which the buyer has the right, but not the obligation, to buy or sell an asset in the future at an agreed-upon price on the agreed date. The option buyer pays the seller an amount called the premium or the price of the opportunity.

* Features:

- Classification: by type of option, including call option and put option, according to the type of contract, including American options and European options.

- Options contracts are traded on both formal and informal markets.

Swap contract

* Definition: A swap contract is a series of maturities settled at different dates in the future at a price agreed between two parties. Conventional swaps do not have cash payments between the two parties, so swaps have an initial value of zero.

* Features:

Swaps made on the principle of clearing will help reduce credit risk by reducing the volume of settlement currencies between the two parties.

Which is the Popular Coffee Derivatives Market?

Of the four contracts mentioned above, the coffee futures contract is the most popular, currently traded on two major global exchanges, the ICE exchange in New York and the Liffe NYSE in London.

- A coffee futures contract is a standardized, binding contract for the delivery or receipt of a particular volume and type of coffee at a specified time in the future at an agreed price. The buyer is obligated to receive the coffee according to the contract terms on a specified date, while the seller is obligated to deliver the coffee.

- Most coffee futures contracts never result in the actual delivery or receipt of the coffee. Instead, contract holders liquidate their positions by clearing transactions in the market. The buyer sells the contract they purchased, and the seller repurchases it, eliminating delivery obligations.

The Margin for The Coffee Futures Contract

The exchange requires market participants to pay initial and incurred margins to secure contract performance. The initial margin is a deposit to ensure that a market participant will fulfill their contractual financial obligations.

Leverage

The appeal of coffee futures trading to investors is leverage. Since futures trades don’t require a full upfront payment (only a margin is required), buyers of coffee futures can reap enormous profits with a leveraged commitment. Assume an investor can buy arabica coffee futures contracts (37,500 lb. each) with a margin of $3,000.

If an investor buys a contract at 150 cents/lb. (costs $56,250 for the contract) and sells the contract when the price of arabica coffee hits 165 cents/lb., that investor will make a profit of $5,625 ( 15 cents x 37,500 lb. = $5,625) – a result equal to 187.5% of the initial margin when the position was liquidated.

That is leverage; it can be a powerful investment tool. Leverage has its downside, of course. If the price of coffee moves in the opposite direction, an investor can lose his entire deposit and much more if standard trading rules and discipline are not followed.

History of Coffee Derivatives Market development in the world

Introduction to the Commodity Derivatives Market

The successes achieved from applying science and technology to agricultural production have promoted the rapid growth of agricultural commodities. Commodities meet the demand of territory and aim to export abundant goods to other regions and countries. However, due to the limited ability to find places to buy and harvest seasonally, the massive supply of goods on the market in a short time has made producers fall into a passive price state—both causing damage to both the supply side and the demand side.

Producers and traders have proactively met before each season to create favorable conditions for the circulation of agricultural products on the market to agree on a price, volume, quality, and delivery time, specifically in the future. But initially, these agreements were still straightforward, small, and without clear and specific standards.

In 1848, the Chicago Board of Trade (CBOT) was established for grain consumption by standardizing quantity and quality and developing long-term contracts for the sale of grain. Futures contracts are traded during this first period. In 1865, the CBOT exchange officially implemented standardized contracts called futures contracts.

The birth of the commodity derivatives market is an inevitable consequence of the market economy, the diversification of trade forms, and international free trade. The derivatives market products are widely applied globally, bringing positive benefits and creating favorable conditions in the general circulation of agricultural commodities and other industrial goods finance. Derivatives have contributed to minimizing risks, transferring risks from producers to the market, helping suppliers feel secure, and focusing their expertise on production.

The world’s first coffee derivatives exchange

The Coffee, Sugar, and Cocoa Exchange (CSCE) was the world’s first coffee, sugar and cocoa futures and options exchange, founded in 1882 as the City Coffee Exchange New York.

Sugar futures contracts were authorized in 1914, and on September 28, 1979, the New York Sugar and Coffee Exchange merged with the New York Cocoa Exchange (founded in 1925) to become the CSCE.

In 1998, CSCE merged with the New York Cotton Exchange as a subsidiary of the New York Stock Exchange (NYBOT). CSCE operates as an independent unit of the NYBOT Exchange that allows the trading of futures and options on coffee, sugar, cocoa, and the S&P commodity index.

In January 2007, NYBOT Exchange merged with Intercontinental Exchange (ICE) in New York and became a subsidiary of ICE Exchange.

Reputable international coffee derivatives exchanges

– The New York Intercontinental Exchange (ICE) trades mainly Arabica coffee;

– London International Financial Futures and Options Exchange (Liffe) is part of the Euronext group, trading mainly robusta coffee;

– Brazilian Mercantile and Futures Exchange (BM&F);

– Singapore Commodity Exchange (SICOM);

– Tokyo Grain Exchange (Tokyo Grain Exchange – TGE).

For arabica coffee, the most traded place is the ICE exchange in New York, and for robusta coffee, the Liffe exchange in London is where derivatives contracts are traded the most. The futures prices listed on the exchanges are different, depending on the supply and demand of each market.

Trade Coffee Futures: Principles of coffee pricing

When the futures contracts mature, the official trading price (FOB – Free on board) will be equal to the futures price on the exchange, plus or minus (discount), with a difference called the difference. The principle of pricing on a differential basis. This difference can be the cost of shipping from the exporting country to the importing country, or it can also be the cost of reduction due to poor quality and other agreed charges.

This pricing principle applies to most coffees worldwide, except some specialty coffees. For example, in a futures transaction where the subject of the contract is coffee from Kenya, the coffee that is judged to be of the best quality will be established through the national auction system, then adjusted in the next transaction based on a different basis.

A coffee futures contract on ICE (Arabica coffee traded in New York)

ICE requires delivery of pure arabica coffee produced in Central and South America, Asian and African countries, or raw arabica coffee from Ethiopia.

- Transaction unit: 37,500 lb (approximately 250 bags)

- Trading hours: 3:30 – 14:00 New York time (Vietnam time: 03:30 pm today to 02:00 am next day)

- Pricing: cents/lb

- Contracts for delivery by month: March, May, July, September, December

- Minimum price fluctuation: 5/100 cents/lb, or $18.75 per contract.

A coffee futures contract on Liffe (Robusta coffee traded in London)

- Trading unit: 10 tons

- Trading hours: 09:00 – 17:30 London time (04:00 pm to 12:30 pm)

- Valuation: USD/ton

- Contracts for delivery by month: January, March, May, September, November

- Minimum price fluctuation: 1 USD/ton or 10 USD per contract

You can view the latest coffee futures contract here.

Keywords: market’s, coffee markets, coffee trading, trading coffee, derivatives trading, derivative, crossref google scholar, google scholar world, product open interest, open interest change, chart open interest, trade coffee futures, coffee market trading, trading coffee CFDs, coffee trading hours, coffee trading strategy, trade, data, price, CFDs, futures, dollar, account, arabica, solutions, green.